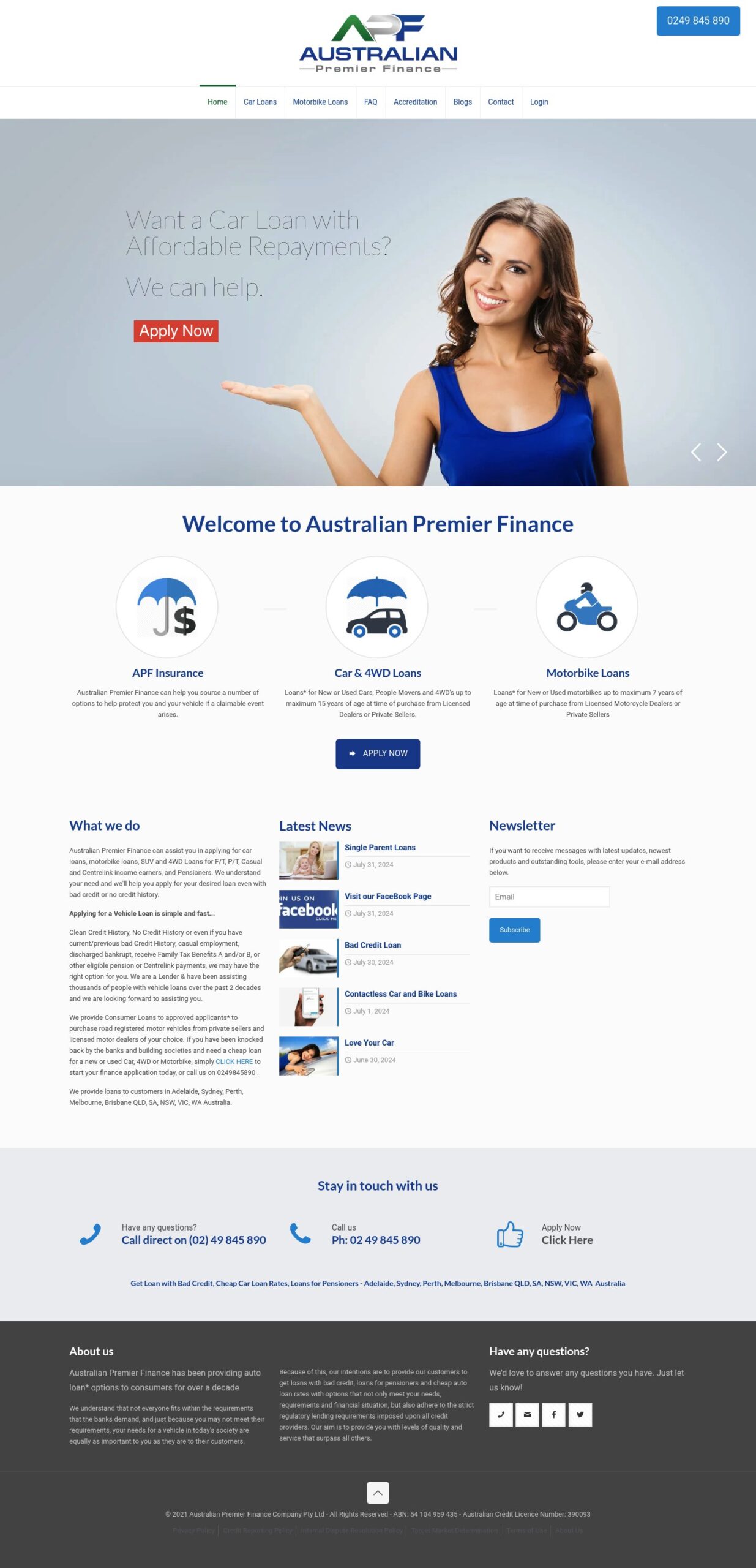

Australianpremierfinance has built real lending experience and regulatory footing from Lemon Tree Passage, NSW, with an 18 60 year claim and thousands of customers across Australia. Despite that history, the combination of a low Google rating (2.8 from 4 reviews) and buried compliance proof leaves pensioner, Centrelink and bad-credit borrowers unsure and walking away. With only about 252 organic visits a month and a national search rank near 418,943, those visitors are not turning into reliable, high-quality online applications.

Your online reputation

2.8

Google star rating

4

Verified reviews

Medium

Reputation strength

Google Business Profile

Your online presence — what the data reveals

AI Visibility

Low

Authority Score

9

out of 100

Organic traffic

252

est. monthly visits

Traffic Trend

+95

%

past 12 months

Organic Keywords

75

ranking terms

Keyword Trend

-46

%

past 12 months

Backlinks

503

total

Paid traffic

0

0 paid campaigns

Digital maturity

Level 2

out of 5

You have a genuine, hard to copy asset in nearly two decades of lending to Australians and a record of helping thousands of customers, and you operate nationally across every state. That operating history and regulatory footing are rare in the subprime consumer auto market and would be costly for a new entrant to reproduce. If the site and proof points are reshaped to match that credibility, those assets can be turned directly into more steady, higher-quality online applications.

How your website scores

TECH STACK

UX OBSERVATIONS

Trust signals exist but are visually demoted. Regulatory identifiers, decade-long experience claims and customer outcomes are buried or small, which causes prospective borrowers to hesitate rather than proceed.

CTA and hierarchy dilute conversion intent. Multiple small, low contrast Apply Now buttons and faint hero copy fail to create a single obvious path to apply, increasing drop off and forcing users to search the page for next steps.

Messaging does not structure buyer decisions. The site presents broad service categories without segmenting offers for bad credit, pensioners or Centrelink recipients, which reduces lead quality and lengthens the sales cycle.

With only about 252 visits a month and a low visibility profile (authority score 9 and national rank ~418,943), the business is getting some interest but not the right kind of confident, ready-to-apply traffic. The 2.8 Google rating from 4 reviews and weak on-page proof points make most visitors pause instead of applying, so real demand and regulatory strength are not translating into reliable leads. The result is erratic enquiry quality and missed opportunities among pensioner, Centrelink and bad-credit borrowers who need immediate reassurance.

The three gaps holding you back

What's possible when these gaps are closed

Lead with your 18 60 year claim and clear compliance markers where visitors look first so people see credibility in seconds, not after hunting the About page. Pair that with a targeted review and testimonial push to address the 2.8 rating from 4 reviews so social proof supports the claim and reduces initial hesitation.

Design distinct landing flows for bad-credit, pensioner and Centrelink applicants so each group sees tailored eligibility language and next steps; this reduces friction and raises lead quality from the ~252 monthly users you already attract. Separate paths also let you match copy and forms to each group’s needs, which will lift the proportion of visitors that start and complete an application.

Simplify the homepage into a single, high-contrast application funnel with one clear call to action and stronger hero copy to improve UX clarity (currently 3), trust (2) and conversion (2). With traffic up from 131 to 255 in the last year, fixing CTA hierarchy and reducing repeated small buttons can turn that traffic growth into consistent, higher-quality applications.

This report was prepared by Redfox Digital using publicly available SEO, UX and reputation data.